Expert Q&A: Accountants Answer Your Most Pressing Tax Questions

To help taxpayers make informed decisions, we asked certified accountants and tax professionals to answer the most commonly asked tax questions. Here’s their expert advice!

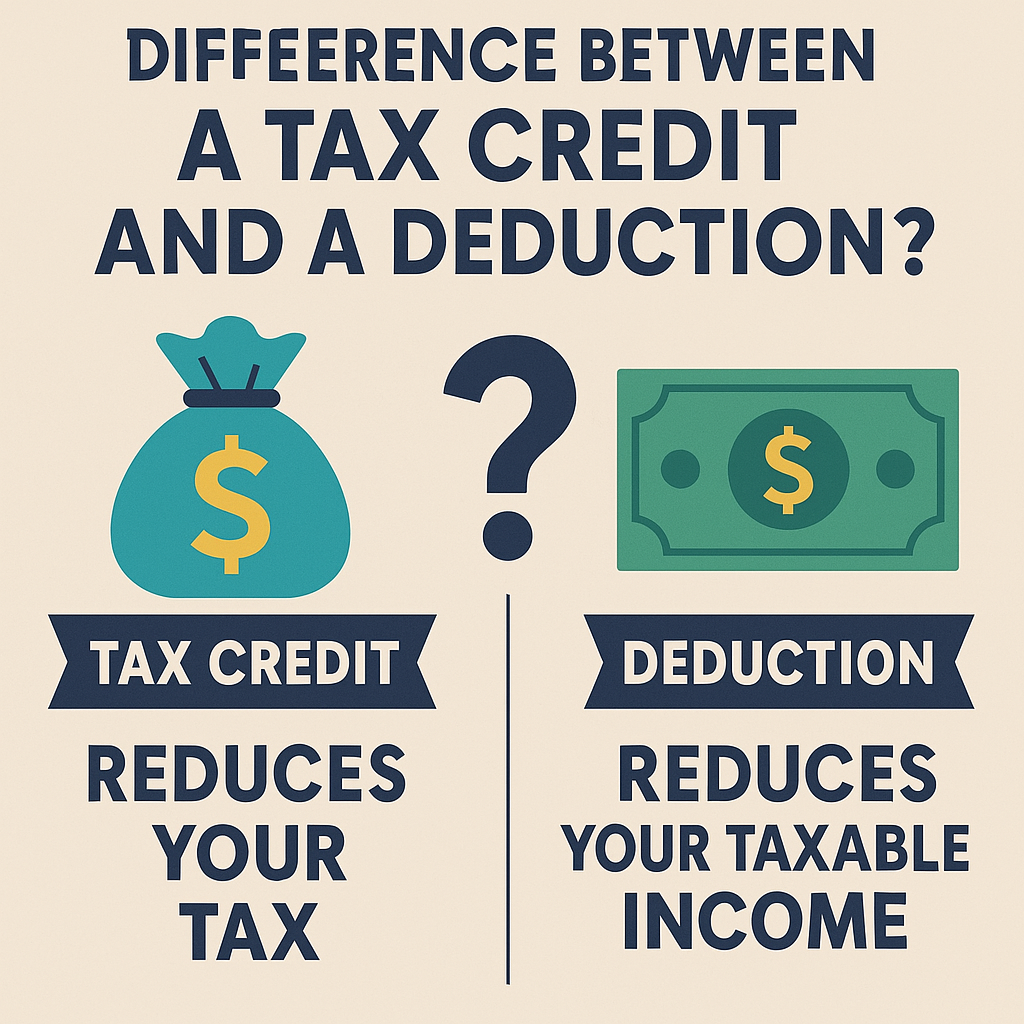

1. What’s the Best Way to Reduce My Taxable Income?

📌 Answer from a CPA: Contributing to a Traditional IRA, 401(k), or HSA is the fastest way to reduce taxable income. Small business owners should maximize business expense deductions and consider an S-Corp election to reduce self-employment taxes.

🔗 Related: IRA 401k Contributions 2024

2. How Can I Avoid an IRS Audit?

📌 Answer from a Tax Attorney: The IRS looks for underreported income, excessive deductions, and cash transactions. Keep detailed records and avoid rounding numbers on your tax return. E-filing reduces errors and audit risk.

🔗 Related: IRS Audit Triggers & How to Avoid an Audit

3. Should I Itemize or Take the Standard Deduction?

📌 Answer from a Tax Consultant: The Standard Deduction is higher for most filers: $13,850 (Single), $27,700 (Married Filing Jointly) in 2024. If your itemized deductions exceed the standard deduction, then itemizing is better.

🔗 Related: Understanding Your 1040 Tax Return

4. Can I Deduct Home Office Expenses?

📌 Answer from a CPA: Yes, if you regularly and exclusively use part of your home for business. You can deduct either actual expenses (mortgage, utilities) or use the simplified $5 per square foot method.

🔗 Related: How Small Business Owners Can Reduce Their Tax Burden

5. How Can I Lower My Capital Gains Tax?

📌 Answer from an Investment Tax Specialist: Use tax-loss harvesting to offset gains. If possible, hold investments for over a year to qualify for lower long-term capital gains tax rates.

🔗 Related: IRS Tax Law Changes for 2025

6. What’s the Best Way to Track Tax Deductions?

📌 Answer from a Tax Preparer: Use accounting software (QuickBooks, Mint, Expensify) or a spreadsheet to log deductible expenses. Keep all receipts and digital records.

🔗 Related: What Documents Do You Need to File Your Taxes?

7. How Can I Fix a Mistake on My Tax Return?

📌 Answer from an IRS Enrolled Agent: If you made an error, file Form 1040-X (Amended Return). You can amend returns for up to three years after the original due date.

🔗 Related: IRS Notices & Letters: What to Do If You Get One

Final Thoughts

Expert tax advice can help you save money, avoid penalties, and make smarter financial decisions. These tips from accountants and tax professionals can guide you toward legal tax-saving strategies.

🚀 Next Steps:

- Consult a CPA or tax professional for personalized tax planning.

- Keep organized records year-round to maximize deductions.

- Stay updated on IRS tax law changes.

🔗 Need more tax guidance? Visit our Tax-Saving Blog.