How Small Business Owners Can Reduce Their Tax Burden

As a small business owner, knowing how to reduce your 1040 tax burden can help you save money and reinvest in your business. Here are proven tax-saving strategies that entrepreneurs and freelancers can use.

1. Maximize Business Expense Deductions

✅ Home Office Deduction – If you use part of your home exclusively for business, you may deduct a portion of rent, utilities, and internet.

✅ Business Vehicle Deduction – Keep a mileage log to claim standard mileage or actual car expenses.

✅ Office Supplies & Equipment – Computers, software, and business-related subscriptions are deductible.

🔗 Related: Year-Round Tax-Saving Strategies

2. Choose the Right Business Structure

✅ Sole Proprietorship – Simplest but offers no legal protection.

✅ LLC (Limited Liability Company) – Helps separate business and personal assets.

✅ S-Corporation (S-Corp) – Can reduce self-employment taxes by paying yourself a salary and taking distributions.

🔗 Related: IRS Forms & Where to Find Them

3. Contribute to a Self-Employed Retirement Plan

✅ SEP IRA – Contribute up to 25% of your net income, reducing taxable income.

✅ Solo 401(k) – Contribute as both employer and employee, with limits up to $69,000 ($76,500 if 50+).

✅ Traditional IRA – Contributions are tax-deductible, lowering taxable income.

🔗 Related: How 2025 Contributions to IRA & 401(k) Can Reduce 2024 Taxes

4. Pay Estimated Taxes to Avoid Penalties

🚨 Self-employed taxpayers must pay quarterly estimated taxes (April, June, September, January).

🚨 Underpayment can result in IRS penalties.

✅ Use IRS Form 1040-ES to calculate and submit estimated tax payments.

🔗 Related: IRS Tax Filing Deadlines & Extensions

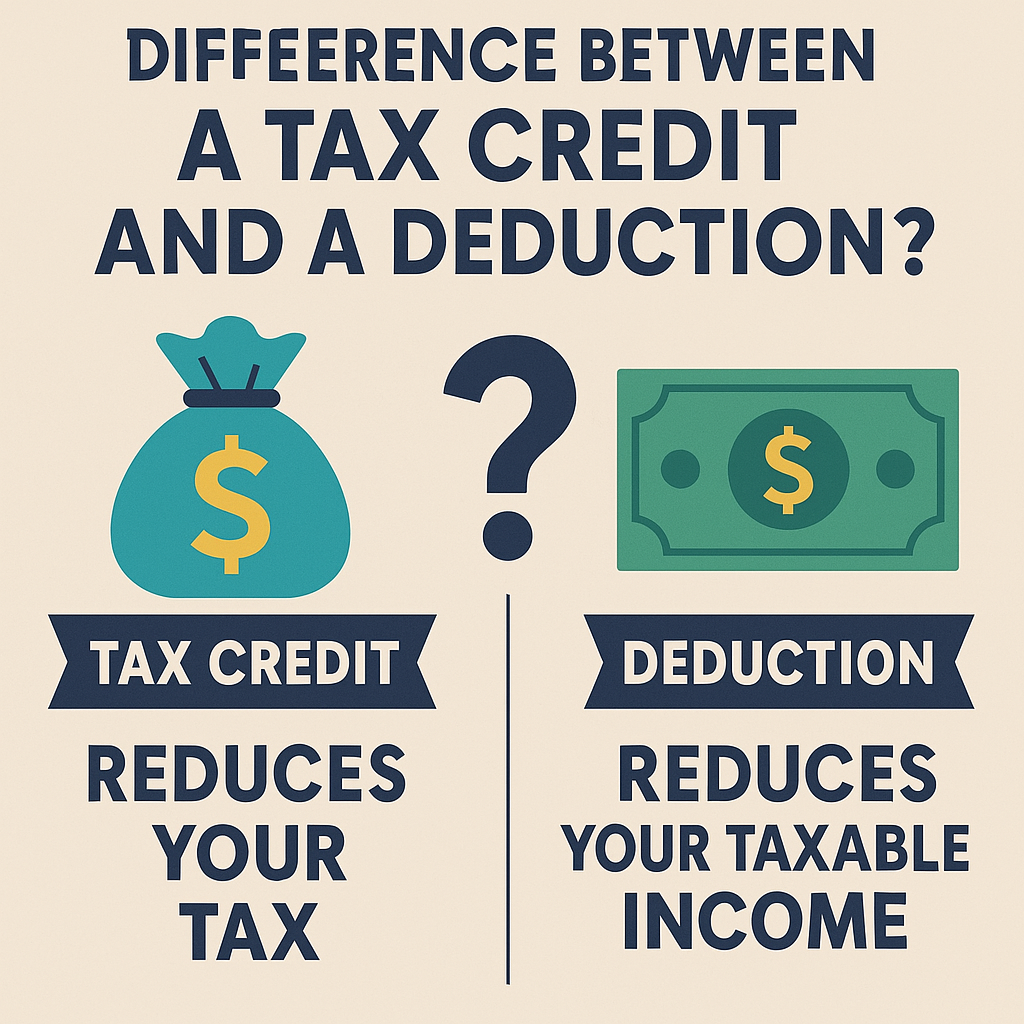

5. Take Advantage of Business Tax Credits

✅ R&D Tax Credit – For businesses investing in research and development.

✅ Work Opportunity Tax Credit (WOTC) – If hiring from certain targeted groups.

✅ Employee Retention Credit (ERC) – Helps businesses that retained employees during economic hardship.

🔗 Related: Your Guide to Tax Credits & Deductions

Final Thoughts

Reducing your small business tax burden requires smart planning, tracking deductions, and utilizing available credits. These strategies can help minimize your tax liability and maximize profits.

🚀 Next Steps:

- Keep detailed expense records year-round.

- Consider a retirement savings plan for tax benefits.

- Ensure estimated taxes are paid on time to avoid penalties.

🔗 Need more tax guidance? Visit our Tax-Saving Blog & Expert Insights.