The financial landscape for student-athletes is changing rapidly. College players can make the most of it — with some planning.

In June 2021, the U.S. Supreme Court changed the landscape for college athletes with a unanimous decision in National Collegiate Athletic Association v. Alston. My colleague Melinda Kibler wrote about this decision in detail at the time. While NCAA v. Alston did not directly deal with name, image and likeness deals, Justice Brett Kavanaugh made clear in a concurrence that bans on NIL deals were living on borrowed time.

In October 2022, NCAA’s Division I board of directors issued a new set of rules, meant to distinguish NIL deals from “pay-for-play” arrangements; the latter remain prohibited. The new rules also limit the financial services and education schools can provide directly to student-athletes. In general, services like tax preparation or contract review are only available if the school offers them to all students, athletes or not.

Beyond these rules, NIL deals are currently governed by a patchwork of state laws. At this writing, 31 states have passed laws governing NIL arrangements, and four states without NIL laws on the books have legislation pending. While Congress has discussed federal NIL legislation in recent years, nationwide legislation remains theoretical. For now, the NCAA specifies that players must abide by state laws where applicable. In states without NIL laws, students may participate in these deals as long as they comply with requirements put in place by their school or conference. These vary but might include limitations such as not accepting endorsement deals with alcohol or tobacco companies.

The ability to enter into name, image and likeness deals offers a variety of advantages to student-athletes. But these deals can also complicate an athlete’s finances in ways he or she may not expect. With some qualified help, self-education and careful planning, players can make the most of the deals that come their way.

Build Your Team

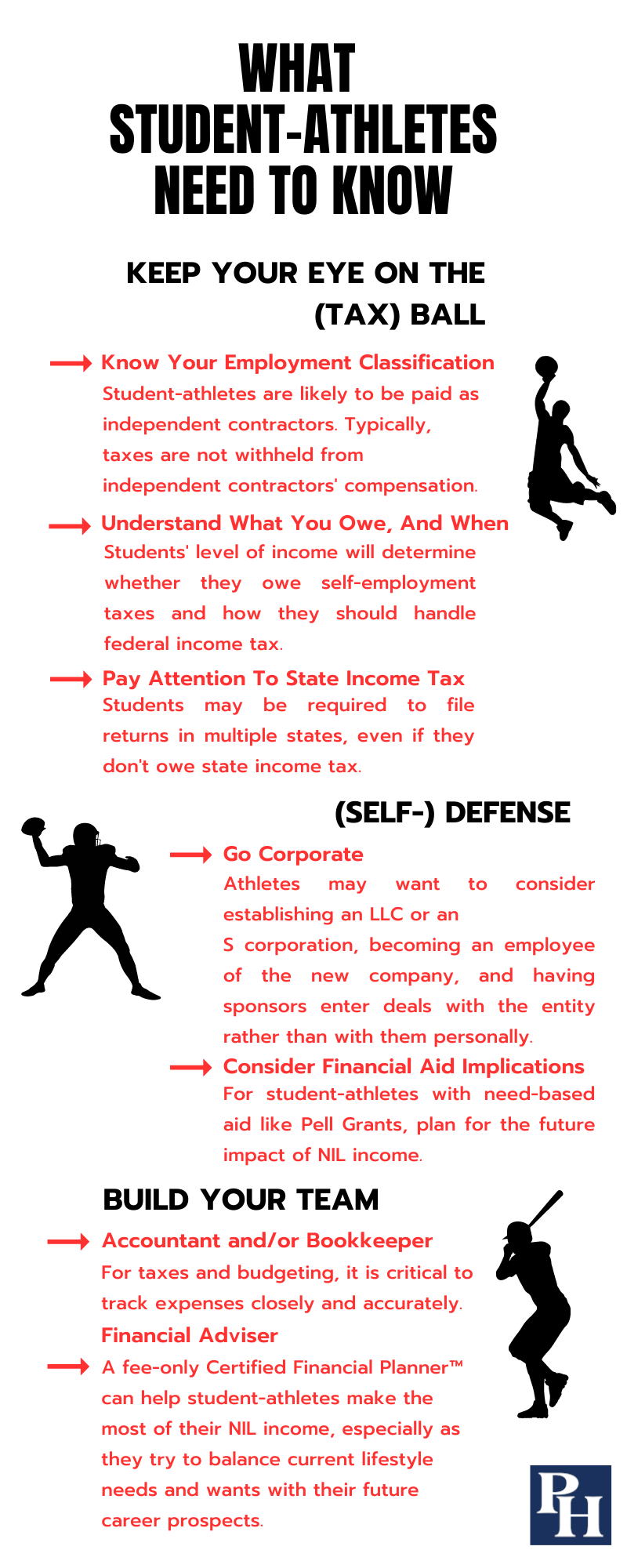

Like an athletic career, a financial strategy benefits from the support of a well-trained team. While the need for professionals will vary, the bigger the NIL deal, the more you can benefit from hiring qualified professionals.

If you are considering hiring a financial planner, you should look for a fee-only adviser. This means the adviser’s interests will be aligned with yours. In addition, an adviser with the Certified Financial Planner™ designation has met rigorous requirements for education, training and ethics. Depending on the planner’s areas of expertise, you may want to hire a separate tax expert or investment adviser, but once you connect with a planner you like, he or she can likely offer suggestions.

Whatever professionals you hire, it is important to make sure you vet them thoroughly. Taking the time to learn more about candidates’ professional background, areas of expertise and communication styles can help you to home in on a team who works for and with you. During the selection process and after, it’s also useful to clarify and remember what each person’s experience makes them best qualified to comment on. A tax professional shouldn’t be your main source of advice when reviewing contracts, just as an attorney who does not specialize in taxes shouldn’t be your principal source of tax planning advice.

In addition to professionals, many college athletes will want or need to work with their parents. If you are a younger player who hasn’t reached the age of majority (often 18, though it can vary by state), you may need your parents or guardians to sign off on contracts or other legal agreements. Beyond this concern, take the time to consider how much parental involvement you want or need, and what forms you would like that support to take. Assuming you have a strong relationship with your parents, they can be an invaluable resource as you learn to manage your financial life.

You may also have access to financial literacy resources through your school. NCAA rules limit which services schools can provide to athletes exclusively. Many schools, however, offer courses and extracurricular support to all students that may benefit athletes considering NIL deals. Resources focused on topics like brand management, marketing and entrepreneurship may be especially helpful.

While brands may want to deal directly with football and basketball players, NIL opportunities exist for students in less high-profile sports, too. In the wake of NCAA v. Alston and states passing NIL laws, organizations called NIL collectives have emerged. NIL collectives are third-party entities that are generally affiliated with, yet independent from, a college or university. The collectives are structured in various ways, but all of them seek to support student-athletes in leveraging their name, image and likeness when they might not be able to do so individually. You can read more about NIL collectives at the IRS Taxpayer Advocate Service’s website. Given the range of structures and rules in play, working with an individual collective may or may not be the right choice for a particular student-athlete. You should investigate the details and, ideally, discuss them with a financial planner before deciding.

Financial Self-Defense

NIL deals can range from amounts that help defray everyday costs of school and training to life-changing amounts of money. Regardless of a deal’s size, remember some basic principles to make sure you avoid common pitfalls.

Setting Up A Business

You may find it useful to treat your endorsement deal, or deals, as a small business. If you decide to pursue this approach, you may want to establish a limited liability company or an S corporation. Setting up shop as a formal business can limit personal liability — for example, in a case of an alleged breach of contract. In some instances, operating as a business can also streamline taxes, though this will depend on the details of your NIL arrangements.

On the other hand, both LLCs and S corps involve ongoing compliance requirements. Setting them up and running them may involve more time and expense than the benefits they offer. If you are curious about setting up an LLC or S corp, you should consult a professional, ideally one with experience working with athletes or entertainers who have similar needs.

Educational Finances

You must include all income, including income from NIL deals, on the Free Application for Federal Student Aid, usually shortened to FAFSA. This means that NIL income can affect need-based financial aid, such as Pell grants. (Income level generally does not affect merit scholarships, including athletic scholarships.) If you receive need-based scholarships and grants, be mindful of these potential effects when considering an endorsement deal.

If you earn a large amount via NIL deals, you may wonder whether you should immediately pay off your student loans. The answer is: It depends. Educational loans, especially those backed by the federal government, often fall into the category of “good debt,” because they create long-term value (in the form of increasing employment prospects and potential future income). Depending on your circumstances, student loans may also offer federal income tax benefits. On the other hand, sometimes becoming debt-free sooner offers greater benefits. A financial adviser can help you to project and compare different scenarios.

Don’t Run Afoul Of The FTC

The Federal Trade Commission sets rules around endorsements and testimonials. These used to mainly apply to celebrities; however, with the advent of social media, influencers and paid placements, the pool of people subject to FTC rules is much wider today.

The FTC stipulates that an endorsement must represent the endorser’s honest opinions or experiences. In other words, if you say that you have used a product, you must have actually used it. You must also make the connection between yourself and the company or product you are endorsing explicit. This connection does not have to be a cash payment. If a brand offers you free or discounted products in exchange for an endorsement, you need to disclose that arrangement. The FTC has even taken issue with where this disclosure appears in a social media post. If you accept deals that include social media posts, be especially careful to comply with existing rules for testimonials to avoid penalties.

Know Where To Draw The Line On IP

Your name, image and likeness inherently belong to you. However, when you wear your school’s uniform, appear on your campus or use your school’s name, you may be including intellectual property that you do not have the right to use without permission.

Now that NIL deals have gone mainstream, many schools are aware of this potential complication. To resolve it, the schools often enter licensing agreements with students (and sometimes alumni) to allow them to use the institution’s trademarks in certain settings or circumstances. Be sure that you understand and respect the limits of these agreements. Schools or teams may also prohibit individual students from entering NIL agreements that conflict with existing sponsorships. It is in your best interest, and your school’s, to make sure such conflicts do not arise.

Contract Warning Signs

As with any contract, pay careful attention before you sign an NIL deal. Read the entire document carefully, and seek clarification on any points that you don’t fully understand.

In general, it is a red flag if a business wants NIL rights without a specified end date. No matter how lucrative the offer, signing away NIL rights indefinitely will rarely make sense. More broadly, when working with a new sponsor, favor relatively short-term agreements, potentially with the option to renew or extend into something longer term if both parties are happy. Hard sell or pressure tactics should be a sign to steer clear.

Finally, it is worth doing some research into a company’s reputation before entering an NIL agreement. Do they have other high-profile endorsement arrangements, and are they with people you would be happy to appear with? How is the business perceived more broadly? The nature of an endorsement deal ties your reputation, at least partially, to the nature of the business offering the deal.

Get A Grip On Taxes

Taxes are among the least exciting but most important factors in handling new sources of income. Especially if you have never dealt with taxes at all, NIL deals can introduce a lot of complexity to your financial life.

Part of this complexity arises because student-athletes who enter NIL agreements are usually considered independent contractors rather than employees. Being classified as a contractor has a variety of effects, some of which you will need to understand long before Tax Day.

You may not be sure when you need to file a federal tax return for the first time. The short answer is that independent contractors who earn at least $400 a year must always file. A variety of other requirements on IRS Form 1040 can also mean you need to file, regardless of your income. That said, if you earn less than the standard deduction ($13,850 for a single taxpayer in tax year 2023), needing to file may not translate into owing federal income tax.

If you are under the age of 24, you should also find out whether your parents plan to claim you as a dependent. If your income provides 50% or more of your overall financial support, you cannot be claimed as a dependent. Assuming this rule is not in play, there is no clear answer as to whether you should remain your parents’ dependent; however, as a dependent, you cannot claim the full standard deduction. Instead, you can claim a lower amount based on your income and filing status.

If you earn at least $600 from NIL deals, you will receive the related tax forms by Jan. 31. These documents, which may include Form 1099-NEC or Form 1099-K, are also issued to the IRS. If you expect to receive a 1099 but it doesn’t arrive, it is still your responsibility to report all income, from NIL deals or anything else, on Form 1040.

Entering into NIL arrangements means you will need to either hire a bookkeeper or keep your own records. If you earn income above the $400 threshold, document and track not only your income, but also any expenses you incur in the course of earning that income. These expenses can include travel and car mileage; meals; internet costs; or advertising expenses, depending on the specifics of the NIL arrangement. Expenses may be deductible to some degree, but it is essential to track them carefully and to keep relevant receipts and documents organized.

Even if you do not owe federal income tax for the year, you will likely need to pay self-employment taxes. These apply to any independent contractors who earn at least $400 for the year. Noncash items like sports equipment, sneakers, or even substantial discounts on products can count as taxable income, too. If the rules apply, you will need to file Schedule C, and potentially Schedule E, along with Schedule SE with your Form 1040. You may also need to pay estimated tax quarterly to avoid penalties for late payment.

In addition to federal income tax and self-employment taxes, student-athletes should be wary of the potential complications caused by state income taxes. In most cases, if your home state is different from the state where you attend college, your home state will have a claim on all your income (assuming your home state levies an income tax). If your school’s state has an income tax, you will likely owe tax on any income you earned there, though reciprocal arrangements can sometimes reduce double taxation.

If you intend to change residency while you are in school — for example, if you are no longer your parents’ dependent and plan to set up a permanent home in the state where you attend school —you will have to take active steps to prove that you have moved. The details are beyond the scope of this article, but see “You Say Goodbye, States Say Hello” by my colleague Paul Jacobs to learn more. For international students, taxes are even more complex. In this situation, it is essential to secure the help of a tax professional with experience in cross-border tax planning.

Make A Game Plan

Once you have a team of professionals and you’ve given Uncle Sam his due, take the time to think strategically about your money. It can be tempting to treat yourself in the wake of a lucrative deal. But balancing income, living expenses, and longer-term wants and needs can let you make the most of your windfall.

Budgeting is about more than just how many dollars you have in your bank account. For example, if you are looking to buy a house, you may have the money for a certain size of down payment — or, in the most lucrative cases, enough money to buy property outright. But it is important to consider how that home will affect your cash flow in the future. Do you have enough to keep up with property taxes, repairs and upkeep, HOA fees, and the many other expenses that come with owning property? A thoughtful budget will allow you to confidently answer that question before you buy.

Similarly, it is important to understand the difference between consumption and investment. Many big-ticket items, such as cars, depreciate the moment you buy them. This does not mean no one should own a car. But it does mean that you should not expect to make back what you paid if you eventually sell it. Rather than scrambling to adjust your budget after-the-fact, planning will let you make major purchases without causing unforeseen financial stress.

Players who secure especially lucrative NIL deals may need to navigate family members hoping for or expecting support. Generosity is a wonderful impulse and not one to avoid outright. But sometimes loved ones may not understand that your newfound income is not unlimited. Since it can be hard to say no in these scenarios, consider asking one of the professionals you hire to be a gatekeeper. Someone such as your financial planner can help you set and stick to boundaries. If you want to make gifts to your loved ones, include them as a component of your overall financial plan, not a series of impulse decisions.

Depending on the size and nature of an NIL deal, you may use it to defray your regular expenses or it may profoundly change your life. Either way, taking the time to get expert advice and make a long-term plan will allow you to make the most of this new opportunity.