The Internal Revenue Service’s Form 1040—the U.S. Individual Income Tax Return—is as much part of America’s fabric as apple pie and baseball.

Granted, you might not consider filing taxes an experience on par with a day at the ballpark. Yet, Form 1040 remains an equally uniting force. In 2022, more than 165 million Americans used this two-page form to file their annual income taxes.

But don’t let the low page count fool you. Form 1040 contains every figure the IRS needs to calculate your tax bill or refund. (If you’re age 65 and older, you can file your annual taxes using Form 1040-SR. The form is identical to Form 1040, but with larger text that makes the form easier to read.)

Whether you file your taxes electronically or by mail, knowing what each section of the form contains can help you gather the information you’ll need to answer questions from your accountant or chosen tax prep software.

To help, Buy Side from WSJ consulted financial and tax experts for insights on Form 1040 for your 2022 taxes—which you’ll file in 2023—including tips to help you report your finances accurately and potentially claim overlooked tax credits.

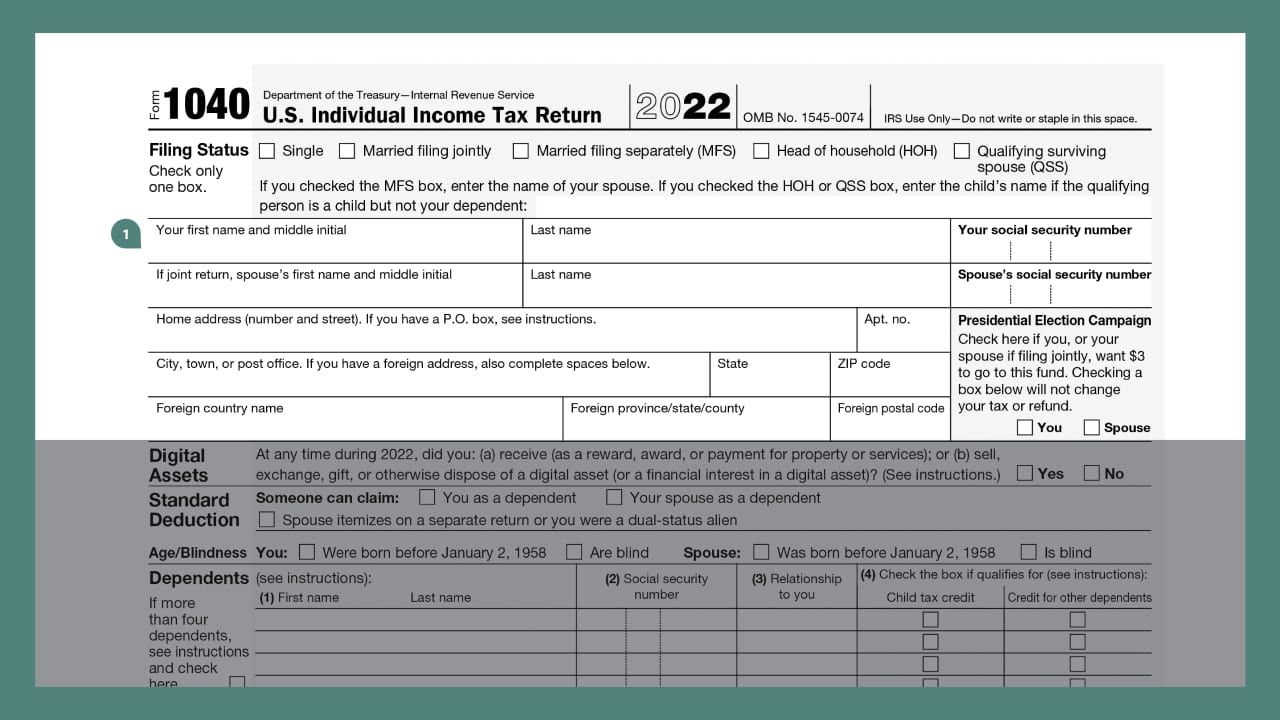

1. Filing status and personal information

At the top of Form 1040, you’ll indicate your filing status and provide your basic personal information.

In the filing status section, you’ll choose one of five possible filing statuses:

- Single

- Married filing jointly

- Married filing separately

- Head of household

- Qualifying surviving spouse

If you select married filing separately, head of household or qualifying surviving spouse, you may need to provide an additional name to support your status selection. However, the rest of the personal information required is straightforward.

This section also lets taxpayers elect a $3 contribution to the Presidential Election Campaign fund. Before 1966, funds for presidential and vice-presidential campaigns were provided solely by individual and corporate donors. However, legislation passed in 1966 added the box to Form 1040 and established a fund that gives qualified presidential candidates public money for primary and general elections.

While counterintuitive, checking the box doesn’t impact your tax bill or refund. Instead, it simply earmarks $3 from federal taxes you’ve already paid to go toward this fund.

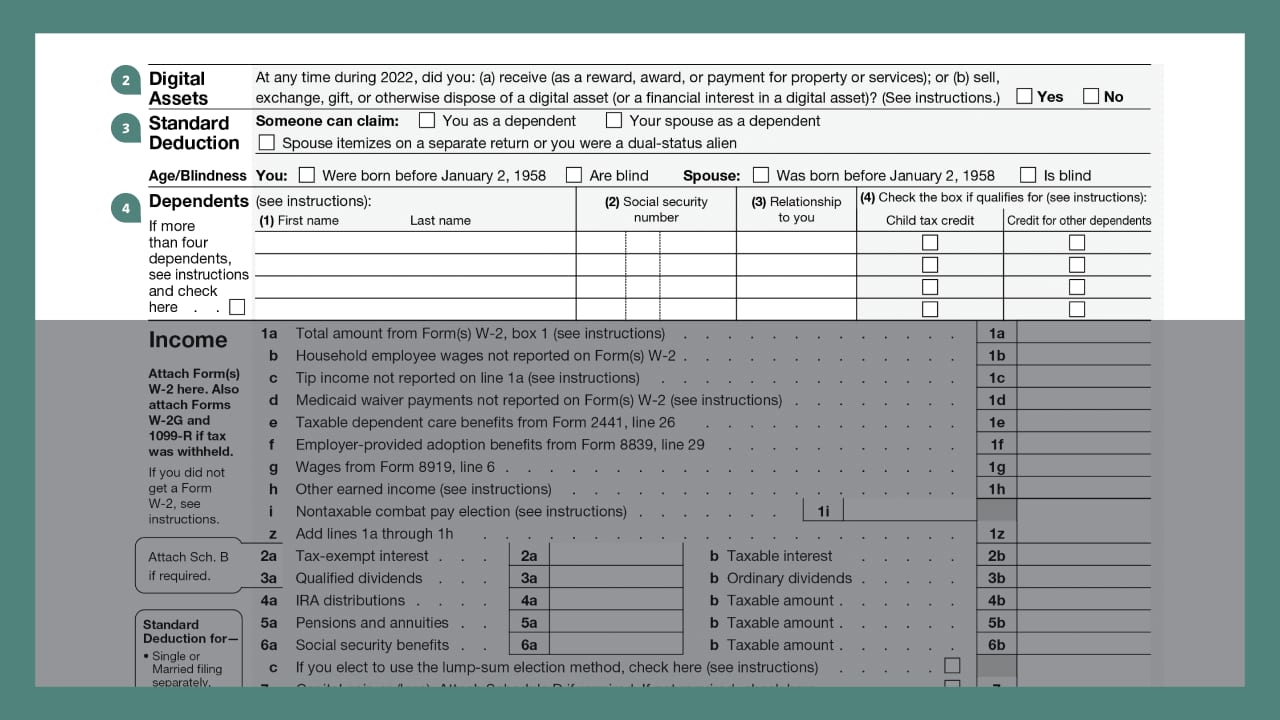

2. Digital assets

In previous years, this section was labeled “virtual currency” but has been renamed “digital assets” and moved to a prominent position before all other financial information on Form 1040.

The reason for the relocation is simple, says Adam Bergman, an alternative assets expert with IRA Financial Group: The IRS is concerned that taxpayers aren’t correctly declaring income derived from digital assets such as cryptocurrencies, nonfungible tokens or stablecoins.

All taxpayers are required to answer this yes or no question. You could be subject to capital-gains taxes if you received, sold, exchanged or otherwise disposed of digital assets in a taxable account in the past year.

If you used cryptocurrency to buy a nondigital asset, that purchase could also be taxable. For instance, if you bought a $10,000 painting with bitcoin purchased for $7,500, you would have to report a taxable gain of $2,500 on your taxes.

For more information, The Wall Street Journal has a guide to cryptocurrency and taxes for the 2022 tax year, including information on taxable transaction types.

3. Standard deduction

In 2017, Congress passed tax changes that bumped the standard deduction to new highs. As a result, most taxpayers now claim the standard deduction—a fixed amount that any taxpayer can use to reduce their taxable income—instead of itemizing.

For the 2022 tax year, the standard deduction is:

- $12,950 for single or married filing separate taxpayers

- $25,900 for married filing jointly

- $19,400 for head of household

If you’re 65 or older or blind, your standard deduction gets a bump. Single and head-of-household filers can add $1,750 to their standard deduction for each criterion they meet. Joint and qualifying surviving spouse filers can add $1,400. So, for example, if you’re a single filer who is both 65 and blind, you can add $3,500 to your standard deduction, making your standard deduction for 2022 a total of $16,450 ($12,950 + $3,500).

If you’re unsure whether the standard deduction or itemized deductions will net you the most significant tax savings, your tax professional—and many DIY tax programs—can help. When in doubt, itemize first and see if your itemized deductions add up to more than the standard deduction for your filing status.

For more information, Buy Side from WSJ has a complete guide to the standard deduction, including dollar amounts for each filing status.

4. Dependents

If you have any dependents for the 2022 tax year, you’ll list them in this section, including a few pieces of additional information. Dependents aren’t limited to children, either. Dependents can be qualifying relatives, including stepchildren, siblings, in-laws or parents.

There is also a box to check if the dependent qualifies for the child tax credit. You can select the child tax credit box if the child was under 17 at the end of 2022. If the child was 17 or older, then select the box for “credit for other dependents.” You’ll calculate your credits elsewhere on the form.

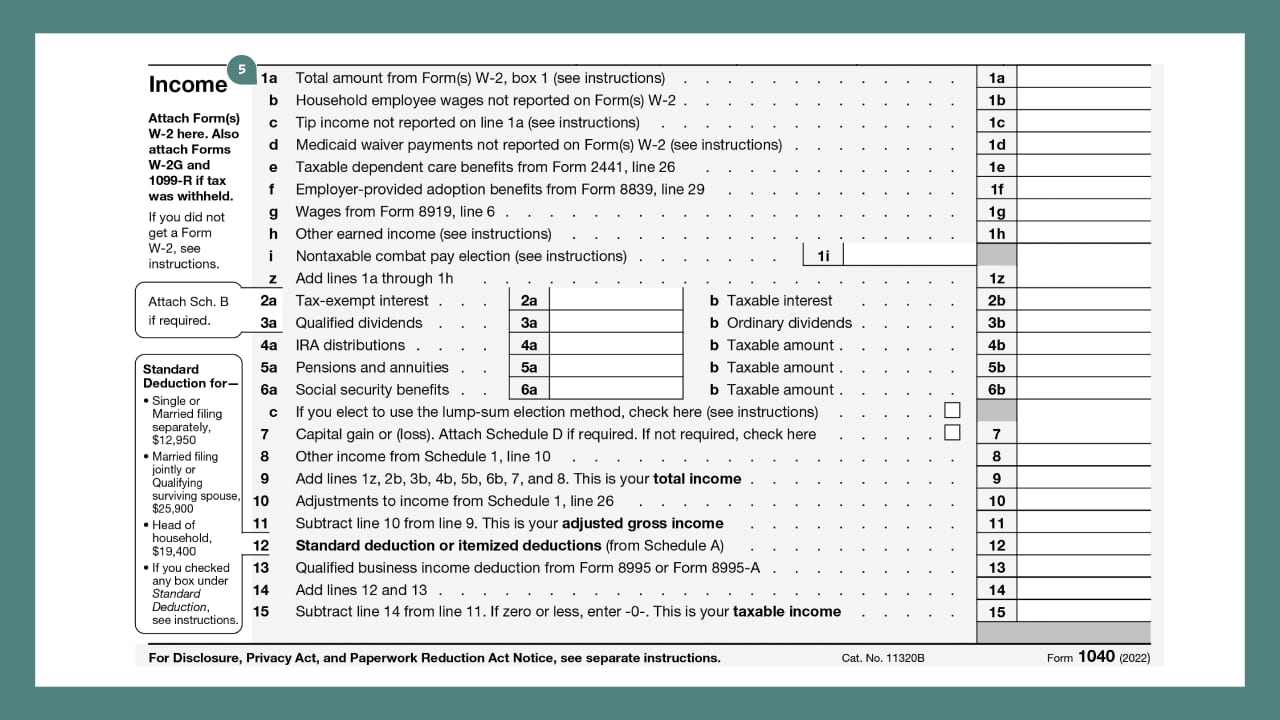

5. Income

In this section, the IRS uses each entry to calculate your adjusted gross income and final taxable income for the year. Some key lines in this section include:

Line 1a: Includes all income from box 1 on your W2 forms, a form you receive at the start of the tax season if you were an employee of any company during the tax year.

Lines 2 a/b — 6 a/b: Includes income from interest, dividends, IRA distributions, pensions, annuities or Social Security benefits.

Line 7: Capital gains or losses from the sale of assets

Line 11: Your adjusted gross income, which is your gross income less IRS-allowed adjustments.

For line 7, capital gains and losses can come from any investment or asset you sell, such as stocks or real estate, says Kendall Meade, a financial planner with online lender and bank SoFi. If you have capital gains to report, “you will probably need to attach Schedule D to your 1040, which allows you to add the detail about each asset sold to total your gains or losses,” Meade says.

Gains or losses from sold real estate are reported on Form 1099-S, which are issued by lenders or real-estate agents. If you sold stocks or other securities, your investment firm reports your gains and losses on a Form 1099-B. Meade notes one final reminder for line 7: You can only realize up to $3,000 in capital gains or losses a year. Losses over $3,000 carry forward to the next year’s taxes.

For instance, say you sold stock and had a capital loss of $5,000 in 2022. You’ll claim the entire loss when you file, but only $3,000 will apply to your 2022 taxes. The remaining $2,000 carries forward and you can claim it on your 2023 return, which you’ll file in 2024.

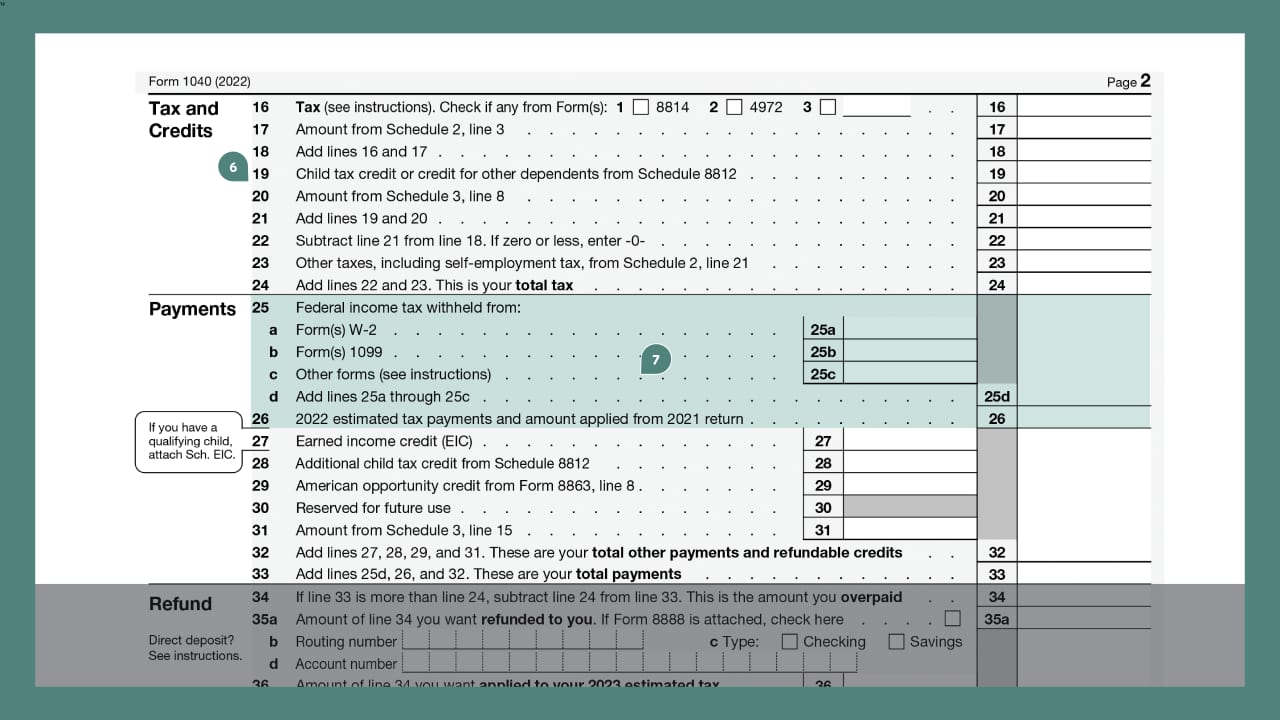

6. Tax and credits

This section tallies your tax liability for the year. Be forewarned: It’s rough going if you’re manually filing your taxes without a tax pro or software to calculate your eligibility.

Since there are numerous tax credits you could qualify for, it is more helpful to zero in on the child tax credit—which has changed substantially since the 2021 tax year.

If you have qualifying children in the Dependents section, your maximum child tax credit for tax years 2022 and 2023 is $2,000 per eligible child. Parents and legal guardians can claim the full credit per child if their modified adjusted gross income for 2022 is less than $200,000 as single filers or $400,000 if filing jointly. The credit starts to phase out at MAGIs above those levels. Any child you claim must be a dependent, have a Social Security number and have been born or adopted in or before 2023. To calculate your credit, you need to complete Schedule 8812, Credits for Qualifying Children and Other Dependents.

The child tax credit reduces your taxable income dollar-for-dollar, and you don’t have to have taxable income to qualify. Those without taxable income can qualify for a tax credit of up to $1,500 per child for 2022 or $1,600 for 2023.

During the pandemic, Congress passed legislation that temporarily increased the child tax credit and offered families the option of receiving part of the credit as monthly payments. However, that legislation expired in late 2022.

7. Payments

In the payments section, Uncle Sam gives you credit for taxes you’ve already paid and additional tax credits that can reduce the tax you owe. To avoid leaving a dime unaccounted for, here’s a line-by-line breakdown of where to find information for lines 25 through 33.

- Line 25a. Enter the combined total of all sums listed in box 2 of your W2s, labeled “federal income tax withheld.”

- Line 25b. You may have had federal taxes withheld from Forms 1099-R (distributions from pensions and annuities), 1099-INT (interest income), 1099-DIV (dividend income), SSA-1099 (Social Security benefits) or RRB-1099 (Railroad Retirement Board benefits).

- Line 25c. If you had taxes withheld on one or more Form W2-G, Certain Gambling Winnings, report the totals from box 4 here. You should also add any taxes withheld on Form 8959, Additional Medicare Tax and Schedule K-1, Partner’s Share of Income, Deductions, Credits, etc.

- Line 26. If you made quarterly estimated tax payments in 2022, you’ll report the total of those payments here.

- Line 27. If you qualify for the earned-income tax credit or EITC, you’ll enter your credit here. There is more detail on this often-missed tax credit to follow.

- Line 28. If you’re eligible for the child tax credit and there is an amount on line 27 of Schedule 8812, enter that amount here.

- Line 29. If you qualify for the American Opportunity Credit, which can help offset the cost of higher-education, enter the amount here.

- Line 31. If you qualify for various other tax credits included on Schedule 3, Additional Credits and Payments, include those credits here.

- Line 33. This is the total taxes you’ve already paid for the tax year.

The IRS estimates that one in five eligible taxpayers miss claiming the EITC, which can be worth up to $6,935. “The people missing it are usually the ones who can least afford to,” says John Vande Guchte, a certified public accountant with Innovia Wealth.

You may qualify for the EITC if:

- Your earned income for the 2022 tax year was less than $59,187.

- Your investment income was $10,300 or less during the tax year 2022.

The income cut off depends on the size of your household (more details are available as part of Buy Side’s guide to adjusted gross income). You also need a valid Social Security number by the due date of your 2022 return (including extensions) and must have been a U.S. citizen or a resident alien for the entire tax year.

Vande Guchte says that some of the reasons people miss claiming the EITC include not knowing it exists, or they may not have qualified in the past but now qualify. He also notes that there’s a myth that self-employed individuals aren’t eligible, but that’s untrue.

The easiest way to see if you qualify is to use the IRS’s online EITC Assistant. You can also use one of the IRS Free File partners to access guided tax preparation and calculate your EITC at no cost, though income limits apply and vary by provider.

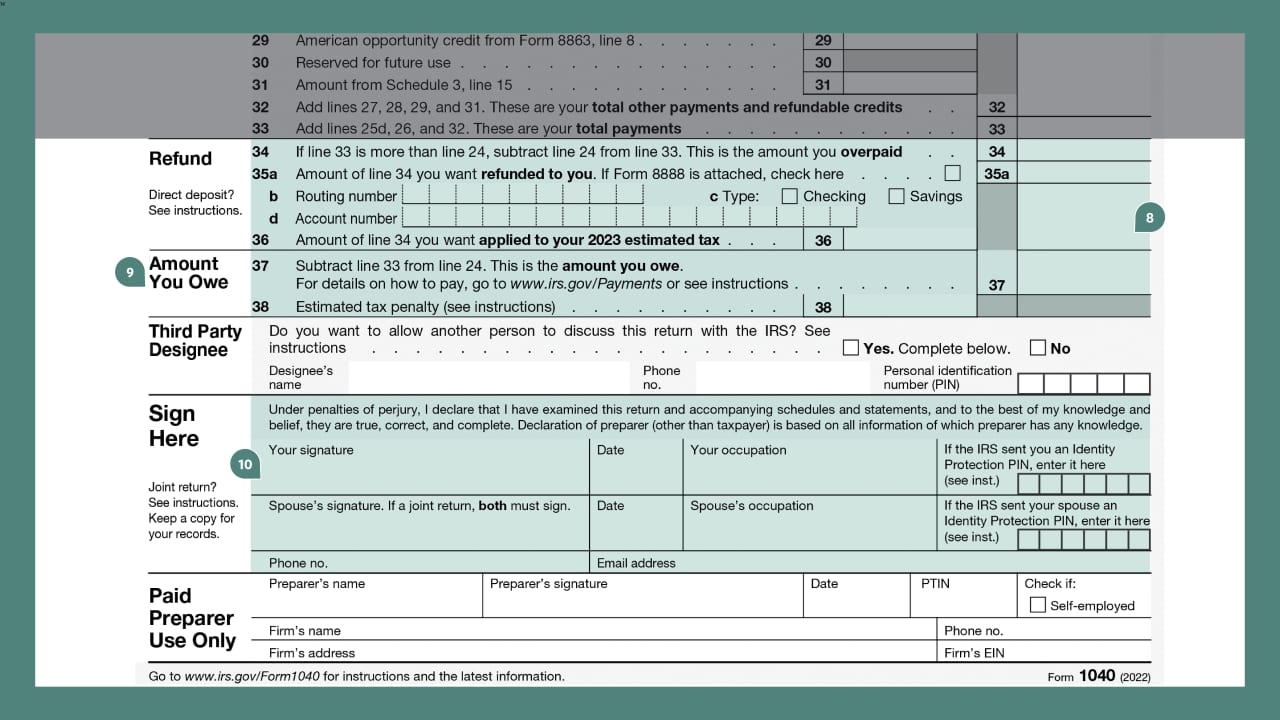

8. Refund

Not everyone will get a refund, those who do will love line 34. This line shows the amount you overpaid for the tax year. In the following line, line 35a, you can indicate how much of that overpayment the IRS should send you as a refund and enter your bank routing and account number to receive your refund electronically.

If you make estimated tax payments throughout the year, you might want some of your overpayment applied to your estimated tax payments for the following year. If so, indicate the amount on line 36.

9. Amount you owe

If you owe taxes, the amount you still need to pay appears on line 37, and you have several options to pay the amount owed. For example, you can send a check when you mail your return, pay by phone, or use the IRS’s payments portal to make an online payment.

If you can’t pay your tax bill in full, don’t panic. You can also use the payment portal to request a payment plan. If you need assistance with your tax bill that a payment plan won’t resolve, the most important thing to do is contact the IRS. Doing so can potentially avoid penalties that can increase the amount you owe.

Line 38 is an estimated tax penalty, which may apply even if you qualify for a refund. You may need to pay a tax penalty if line 37 is more than $1,000 or if you didn’t make the required estimated tax payments by their due date. If you think you may owe a penalty, use Form 2210 to determine whether you owe a penalty and the amount.

10. Completing your return

The bottom of Form 1040, page 2, collects required signatures—from you, your spouse and your tax pro if you used one—and lets you name someone who can discuss your return with the IRS, a third-party designee.

If you’re filing by mail, sign your return and make a copy for your records. If you owe taxes, enclose a check or money order or use the IRS payments portal to arrange payment. If filing electronically, your tax pro or tax prep software will have you sign Form 8879, IRS e-file Signature Authorization.

Signatures on Form 8879 can be electronic or physical, and once the form is signed you can submit your return for e-filing. Either way, you’ve filed your taxes and can relax with a nice slice of pie or a day at the ballpark.

The advice, recommendations or rankings expressed in this article are those of the Buy Side from WSJ editorial team, and have not been reviewed or endorsed by our commercial partners.